Explore My Research

My research focuses on migration, entrepreneurship, and political economy, with an emphasis on how institutions, policy environments, and economic incentives shape individual behavior and long-run development outcomes. Click a topic below to filter.

Migration R&R

Did the Syrian Refugee Crisis impact European economic freedom?

Using synthetic control methods, we find no evidence that the Syrian refugee surge eroded economic freedom in Germany, Austria, or Sweden.

Migration Entrepreneurship

Working Paper

From Das Kapital to Venture Capital: Cuban Entrepreneurial Elites Exiled in South Florida

Coming soon…

Entrepreneurship Working Paper

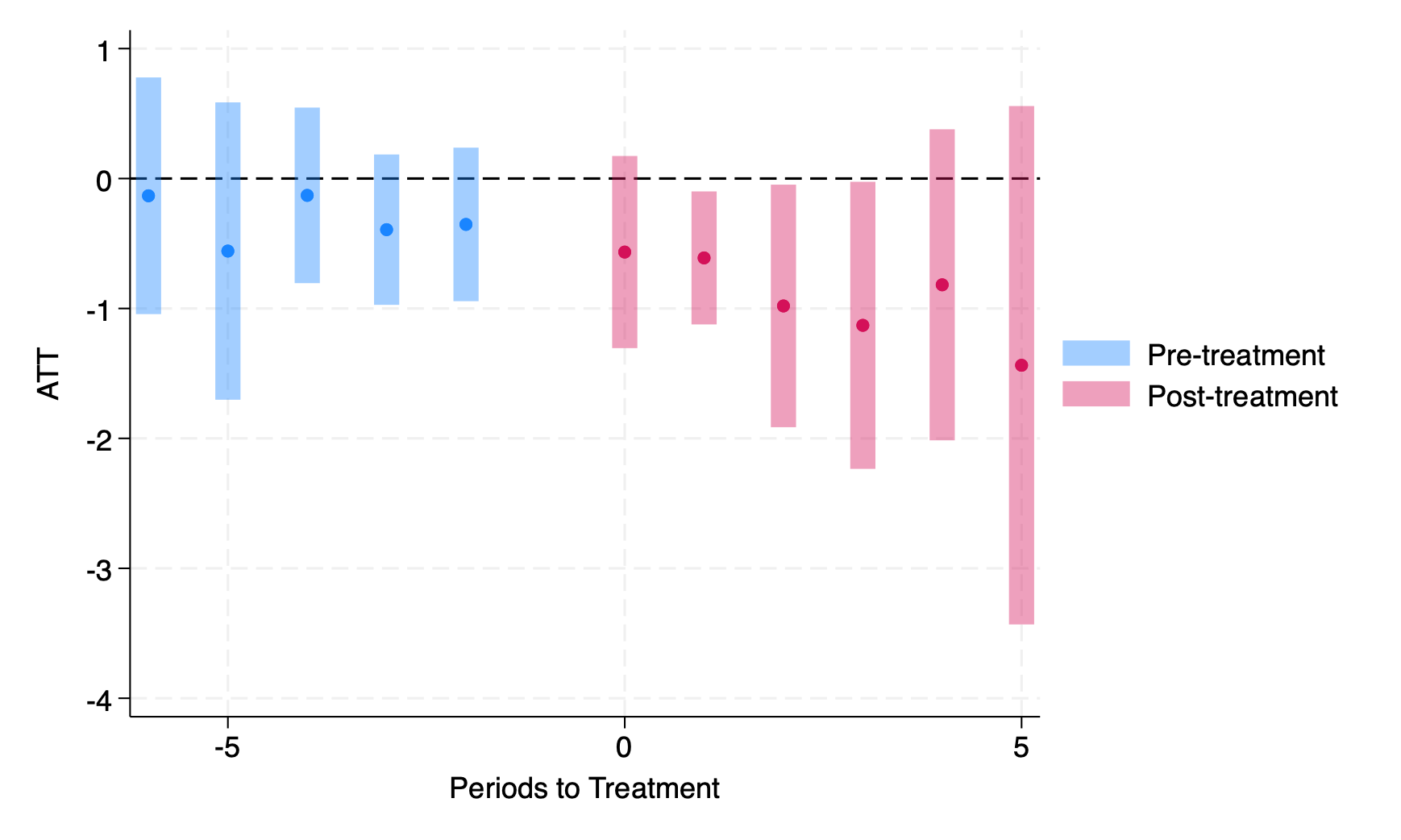

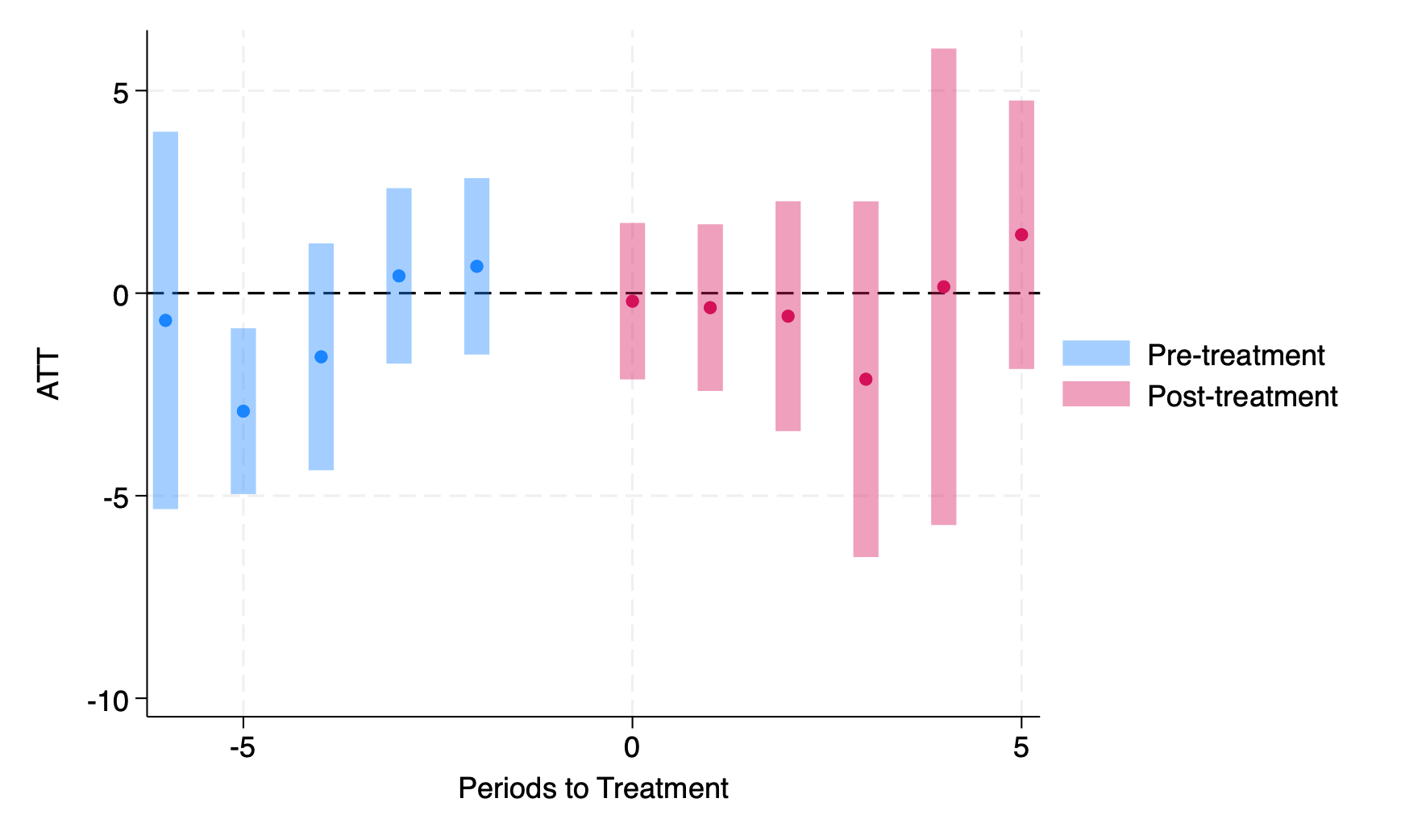

Do corruption reforms spur entrepreneurship?

Sustained anti-corruption reforms have no statistically significant effect on any measure of entrepreneurship, suggesting growth gains flow through other channels.

Read more

Pavlik et al. (2023) showed that sustained anti-corruption reforms cause economic growth, but through what channel? This paper applies the Callaway and Sant’Anna (2021) DiD estimator, which properly handles staggered treatment adoption, to test whether reducing corruption boosts business creation. Treatment is defined as a sustained 5-year improvement of more than 0.20 in the World Bank’s Control of Corruption index.

The analysis uses two complementary datasets: the World Bank Group Entrepreneurship Survey (formal firm registrations per 1,000 working-age people, 20 treated countries) and the Global Entrepreneurship Monitor (total, opportunity-driven, and necessity-driven TEA, 10 treated countries).

Formal registrations show a slight negative point estimate (ATT = −0.70, s.e. = 0.54). Total TEA is essentially flat (ATT = −0.51, s.e. = 1.42). Necessity-driven TEA shows the largest decline (−2.68) but remains insignificant.

The divergence between formal data (slight decline) and GEM data (no change) suggests reforms may temporarily reshape the form of entrepreneurship, shifting activity between formal and informal sectors, without changing overall business creation rates. The growth benefits documented by Pavlik et al. must therefore flow through other channels: investment, human capital, or productivity improvements within existing firms.

Migration Published

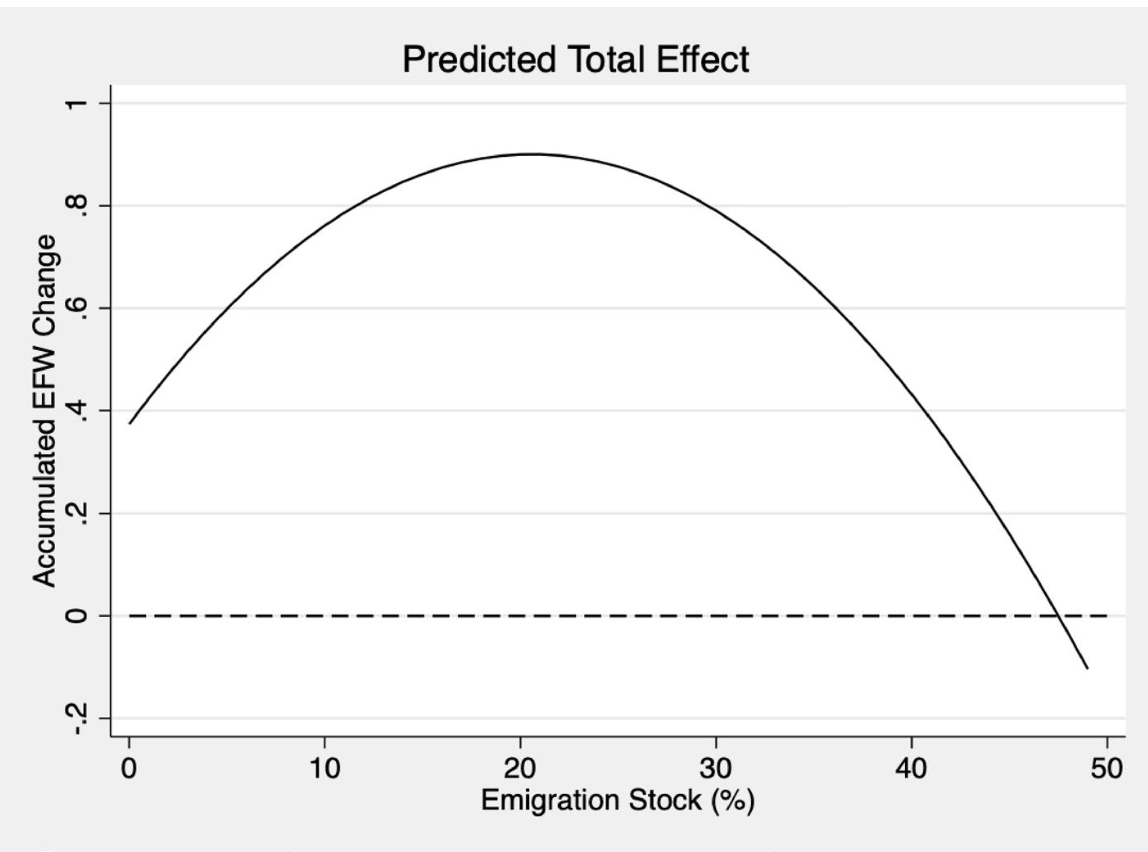

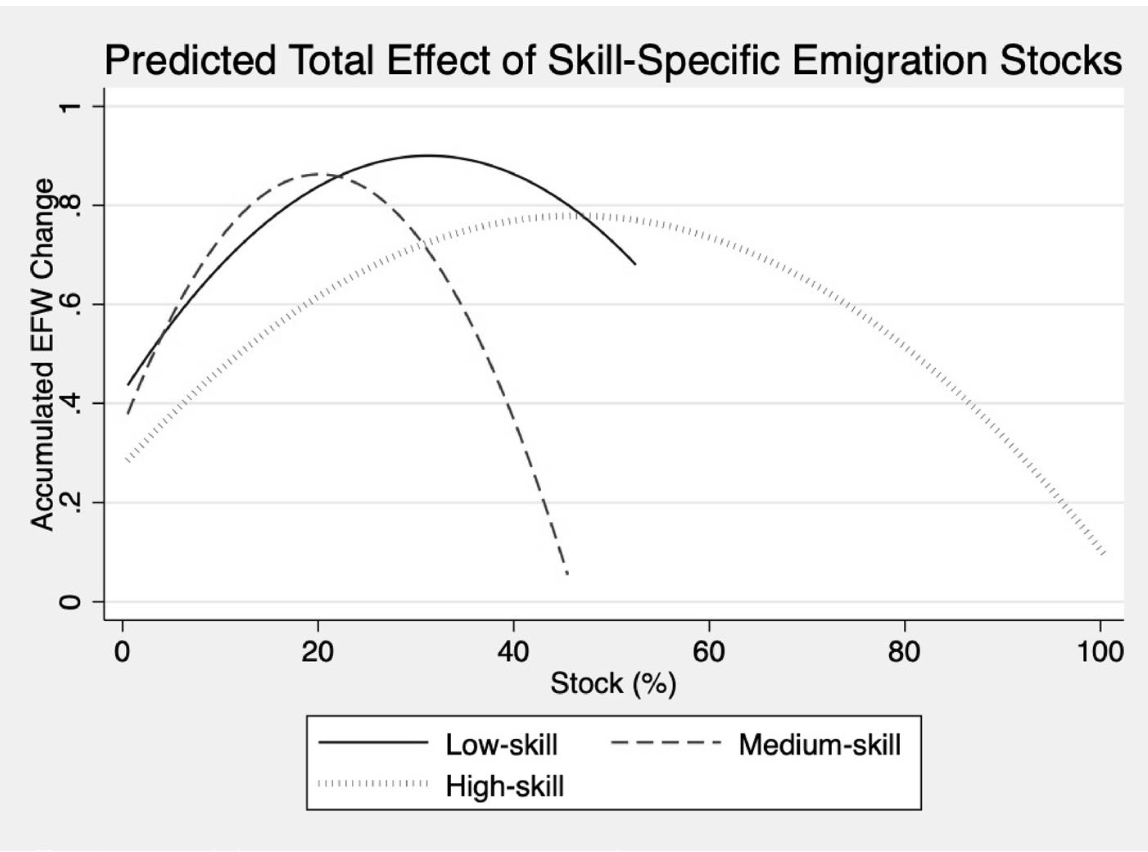

Emigration and origin country economic institutions

Moderate emigration improves origin-country economic institutions through an inverted-U relationship, driven by medium- and high-skill emigrant stocks.

Read more

Drawing on public choice theory and Hirschman’s exit-voice framework, this paper identifies four channels through which emigration affects origin-country institutions: the absence channel, the prospect channel, the diaspora channel, and the return channel. These predict an inverted-U: moderate emigration improves institutions, but extreme levels deplete human capital and civic participation.

We test this using panel data on emigration from 132 countries to 20 OECD destinations (1980-2010) and the Economic Freedom of the World (EFW) index. Specifications include two-way fixed effects, quadratic terms, and skill-specific disaggregation.

The results confirm the inverted-U hypothesis. Emigrant stocks are positively and significantly associated with improvements in economic freedom, peaking at about 20% of the population abroad (a 0.90-point improvement on the 10-point EFW scale). Only above 47% does the effect turn negative, and only Guyana exceeds that threshold.

Medium- and high-skill emigrant stocks drive the result. High-skill emigration never turns negative within the observed range, suggesting persistent institutional spillovers. The policy implication: allowing greater emigration from low-freedom countries could promote development through institutional improvement, a channel that adds to the already large estimated gains from freer migration.

Entrepreneurship Published

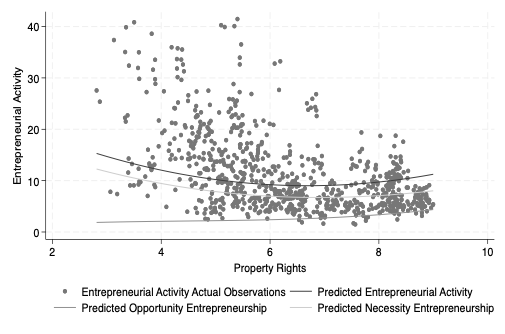

Property rights and entrepreneurship

Property rights and total entrepreneurship follow a U-shaped relationship: necessity entrepreneurship falls first, then opportunity entrepreneurship rises.

Read more

The literature assumes a linear relationship between property rights and entrepreneurship. This paper challenges that assumption, proposing and testing a U-shaped (nonlinear) relationship. At low levels, necessity-driven entrepreneurship dominates. As institutions improve, formal jobs absorb this activity. Beyond a threshold, opportunity-driven entrepreneurship accelerates and total activity rises again.

The empirical analysis uses panel data from the Global Entrepreneurship Monitor across 90 countries (2004-2018, 822 observations), paired with the Fraser Institute’s Legal System and Property Rights sub-index. The baseline is a random-effects panel regression of TEA on property rights and its square, controlling for GDP per capita, GDP growth, unemployment, and population growth.

The results confirm the U-shape. The linear term is negative and significant (−5.590, p<0.01), the quadratic term positive and significant (+0.418, p<0.05), with a Wald test confirming the squared term matters (p = 0.011). The minimum occurs at a score of approximately 6.69, comparable to Chile. A purely linear specification yields an insignificant coefficient, demonstrating it misses the true relationship entirely.

Separate regressions reveal the mechanism: each additional point in property rights increases opportunity entrepreneurship by 0.0432 pp (p<0.01) while decreasing necessity entrepreneurship by 0.0142 pp (p<0.01). The gain in opportunity ventures is more than three times the decline in necessity ventures. Results are robust to using the World Bank’s Rule of Law index instead.

The policy implication: policymakers should not be discouraged if modest institutional improvements do not immediately produce a surge in business creation. The initial decline reflects a healthy transition away from survivalist informality. The payoff comes with sustained reform past the trough.

Fiscal & Monetary Policy Working Paper

Debt Constraints in Emerging Economies: Synthetic Control Evidence from Guatemala

Guatemala’s fiscal rules reduced central bank lending but did not produce genuine fiscal discipline; the debt-to-GDP improvement was driven by inflation, not austerity.